Build to matter

Ready to work together?

If you’re an established or growing business ambitious about shaping your market—not just your margins—we’d be delighted to talk.

Perigon’s 2025 Banking Barometer benchmarks 57 UK banks on ESG, strategy, and GenAI maturity - revealing progress, gaps, and future risks.

Emma Walford

September 2, 2025

.png)

Our 2025 Banking Barometer is live - our third comprehensive benchmark of UK banks, building societies and fintechs. This year is bigger and more useful for three reasons:

Leaders are being pulled in multiple directions, not least tightening sustainability expectations and the AI wave. Articulating clear strategic priorities that withstand scrutiny can help navigate the noise; failure to do so can add to the drag. Our Barometer distils how 57 UK institutions (from local building societies to global banks) are actually responding, based on what they disclose in their annual reports.

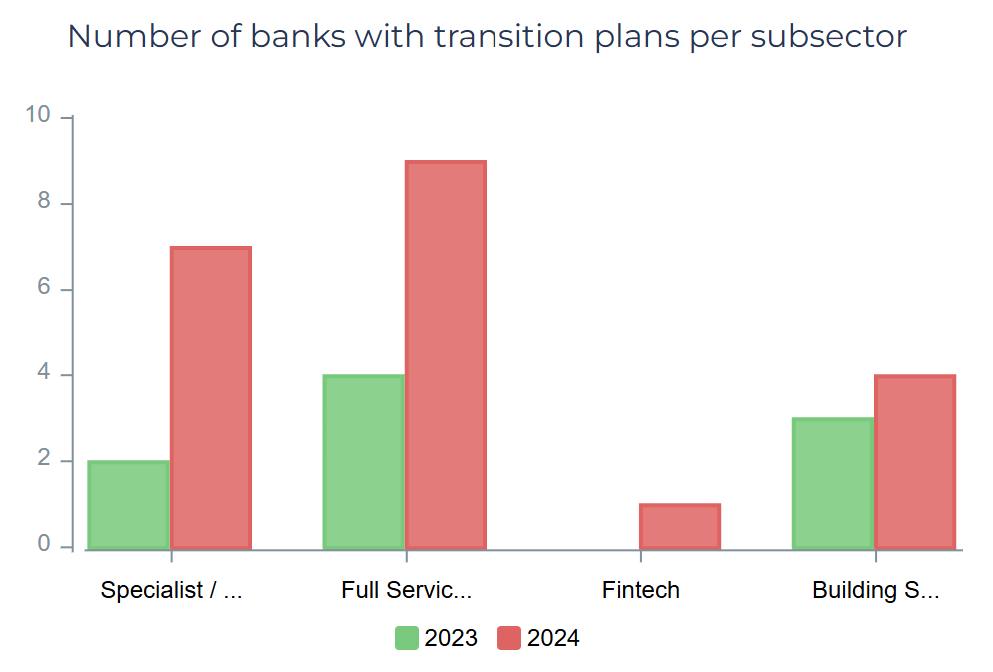

The average sustainability section in annual reports is now 21 pages (up from 16). Much of the uplift comes from CSRD-driven reporting by Irish banks in the cohort - an early signal for UK institutions preparing for UK Sustainability Reporting Standards. Transition plans are moving mainstream: 90% of full-service banks now have climate transition plans (and 33% of challengers/specialists). Nature-related investment activity is quietly ticking up - banks are just getting on with it without a major regulatory push or song and dance - while use of carbon credits to offset emissions is declining.

49% of banks now report financed emissions, up 12 percentage points year-on-year (seven new reporters in FY24). Scope 1 and 2 emissions continue to fall (as expected from estate and fleet decarbonisation). The surprise riser: business travel emissions intensity, particularly among fintechs.

Climate targets are becoming more common and clearer. 65% of banks now have Net Zero targets (vs 34% last year), increasingly standardised to 2050. The real quality shift is in interim targets - especially among fintechs, signalling operational maturity and, we suspect, pre-IPO discipline.

As banks prepare for the FY25 reporting season, three principles are important to remember:

Many banks articulate a focused set strategic priorities; weaknesses include vague timelines andparallel, unintegrated strategies (e.g. sustainability or technology). Larger banks generally score higher on our strategy communication framework - greater in-house capacity and consulting spend likely help. Controlling for size, fintechs outperform on clarity and ambition while building societies tend to underperform.

And because life is too short to be serious all the time, we’ve mapped the different strategy profiles to a set of familiar car archetypes. Are you a Vauxhall Astra or a Reliant Robin of strategy - check our webapp to see which best describes your approach to strategy.

One in four banks made no mention of AI in their FY24 annual reports. And 84% showed no evidence of strategic thinking about AI beyond narrow cost efficiency. That’s a risk. We view AI as a general-purpose technology that will reshape customer experience, risk, operations and growth models. While lots can change in a few months and these disclosures were backwards-looking, we had expected more commentary about strategic AI capability building (talent, data foundations, governance, model risk) vs a few side notes about customer service chat bots.

We spend the (significant) time and effort on the Banking Barometer each year to help you pressure-test your plans and your approach to disclosures. Use it to benchmark where you’re ahead, where there are gaps to close in year and where you might focus future efforts. We are always happy to discuss the findings and welcome any challenge.

TL;DR: Perigon’s 2025 Banking Barometer is live, providing an interactive benchmark on UK banks’ approaches to sustainability, strategy and AI. Disclosures are maturing, the AI divide is widening, and strategy clarity is mixed. Explore the UK financial services industry and where your bank stands.

© Perigon Partners Ltd. All rights reserved. Perigon Partners Ltd is a Scottish-registered company (SC716835).